You’ve heard the whispers on YouTube, seen the threads on Reddit, and maybe a friend mentioned it over coffee: “velocity banking.” It sounds almost like a financial magic trick—a secret strategy to pay off your 30-year mortgage in a fraction of the time. Naturally, your next step was to search for a velocity banking calculator, hoping to plug in your numbers and see the magic for yourself.

But what if the most powerful calculator isn’t a tool you find online, but a concept you understand in your head?

That’s what this guide is all about. Instead of giving you a simple box to type in, we’re going to pop the hood and show you exactly how the engine works. We’ll break down the math, demystify the inputs, and walk through the strategy step-by-step. By the end, you won’t need a fancy spreadsheet; you’ll have the essential knowledge to evaluate if this powerful—and risky—strategy is right for you.

- Before You Click “Calculate”: What is Velocity Banking, Really?

- Peeking Under the Hood: The Core Components of Any Velocity Banking Calculator

- How to Calculate Velocity Banking Manually: A Step-by-Step Example

- Is Velocity Banking Worth It? The Unbiased Pros and Cons

- Velocity Banking Calculators vs. Reality: Apps, Spreadsheets, and Red Flags

- Frequently Asked Questions (FAQ)

- The Final Verdict: Is The Knowledge Your Best Calculator?

Before You Click “Calculate”: What is Velocity Banking, Really?

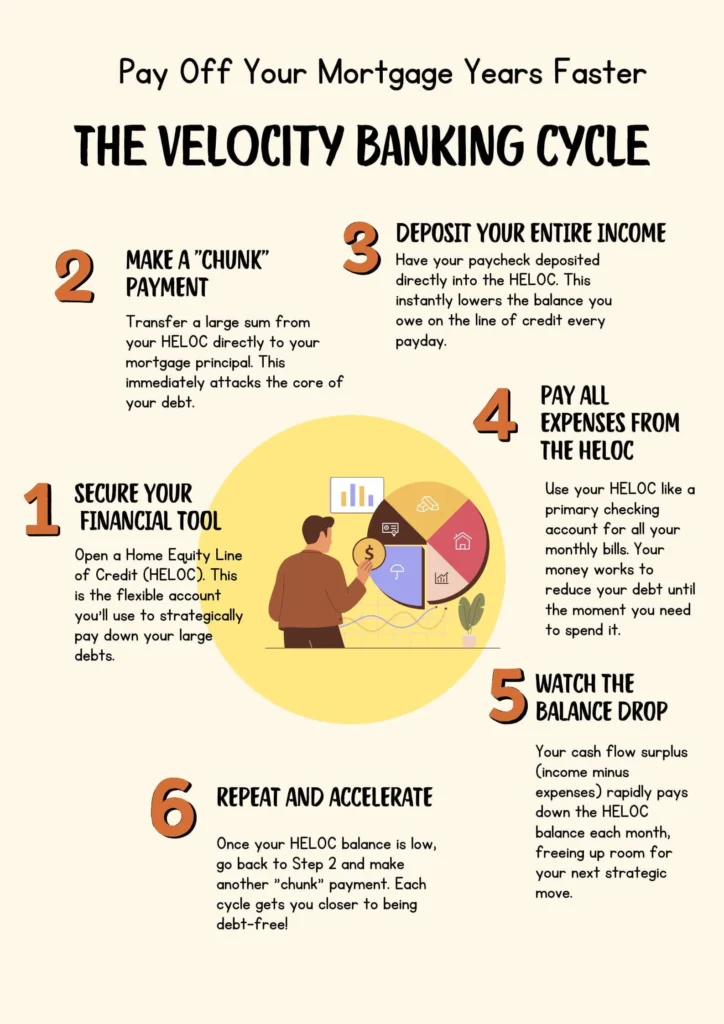

At its core, the velocity banking strategy is about using a simple financial tool in a very clever way. It’s a method of using a revolving line of credit, most often a Home Equity Line of Credit (HELOC), as your primary checking and savings account. The goal is to use your cash flow to rapidly pay down high-interest, long-term debt like a mortgage.

Instead of your paycheck sitting in a low-interest checking account, it goes directly into your HELOC. This immediately reduces the balance you owe on that line of credit. Then, you pay all your monthly expenses—groceries, utilities, car payments—out of the same HELOC. The difference between your income and expenses remains in the HELOC, continuously suppressing the balance and minimizing the interest you pay on it.

This creates “chunks” of available credit that you can then use to make large, strategic principal payments on your mortgage. If you’re new to the core concept, our essential guide to what is velocity banking provides the perfect foundation before we dive into the numbers. The key takeaway is that you’re making your money work harder every single day, not just on payday.

Peeking Under the Hood: The Core Components of Any Velocity Banking Calculator

Any online tool, from a simple web form to a complex velocity banking calculator excel spreadsheet, is built on the same fundamental inputs. Understanding these components is the first step to calculating the potential of this strategy for yourself.

Input #1: Your Primary Debt (The Mortgage)

This is the mountain you’re trying to move. The calculator needs to know its exact size and shape.

- Principal Balance: The total amount you still owe on your mortgage. This is the starting line.

- Interest Rate: The percentage you’re being charged on the loan. A higher rate means you’re losing more money to interest over time, making strategies like velocity banking more appealing.

- Remaining Term: How many years are left on your loan? This helps calculate your current amortization schedule—the slow, traditional path to payoff—which serves as the baseline for comparison.

Input #2: Your Financial Lever (The HELOC)

This is the tool you’ll use to move the mountain. A velocity banking HELOC strategy lives or dies by the terms of this line of credit.

- HELOC Limit: The maximum amount you can borrow. This determines the size of the “chunks” you can throw at your mortgage.

- Variable Interest Rate: This is a critical risk factor. Unlike your fixed-rate mortgage, most HELOC rates are variable, meaning they can rise and fall with the market. A reliable calculator must account for this interest, as it’s a new cost you’re introducing. Many overly optimistic tools conveniently downplay this.

- Initial Draw: This is the amount you’ll pull from the HELOC to make your first large payment on the mortgage.

Input #3: Your Cash Flow (Income vs. Expenses)

This is the fuel for your financial engine. It’s the “velocity” in velocity banking.

- Monthly Income (Net): Your take-home pay after taxes. This is the total amount you have to work with each month.

- Monthly Expenses: Every dollar you spend, from your electric bill to your morning coffee. The more accurate this number, the more realistic your calculation will be.

The difference between your income and expenses is your “cash flow surplus.” In traditional budgeting, this might go into a savings account. In velocity banking, this surplus is what aggressively pays down your HELOC balance month after month, creating more room for your next chunk payment.

Input #4: The “Chunk” Amount

This is where the strategy happens. A “chunk” is a significant, lump-sum payment you make to your mortgage principal, paid for by drawing from your HELOC. The size of this chunk is a strategic decision. A good velocity banking calculator would allow you to model different chunk sizes to see how they impact your payoff timeline. For instance, would a single $20,000 chunk now be more effective than two $10,000 chunks over the next year? This is the kind of question that understanding the mechanics helps you answer.

How to Calculate Velocity Banking Manually: A Step-by-Step Example

Enough theory. Let’s see how this works in the real world. Forget the apps and spreadsheets for a moment. We’re going to do a manual calculation.

Let’s meet Sarah, a project manager living in Austin. She’s tired of seeing so much of her payment go to interest and wants to see if velocity banking is worth it.

Step 1: Establish the Baseline

First, we need to know Sarah’s current financial picture.

- Mortgage Balance: $300,000

- Mortgage Interest Rate: 6.0% (Fixed)

- HELOC Limit: $50,000

- HELOC Interest Rate: 8.5% (Variable)

- Monthly Net Income: $6,000

- Monthly Essential Expenses: $4,500

- Monthly Cash Flow Surplus: $1,500 (Calculation: $6,000 – $4,500)

Step 2: The First “Chunk” and Interest Calculation

Sarah decides to make an aggressive first move. She takes a $20,000 chunk from her HELOC and applies it directly to her mortgage principal.

- New Mortgage Balance: $280,000 (Calculation: $300,000 – $20,000)

- New HELOC Balance: $20,000

Instantly, she has knocked years off her mortgage amortization schedule. But she’s also opened a new $20,000 debt. Now, we must calculate the first month’s interest on that HELOC.

- HELOC Interest Calculation: (

20,000x8.520,000x8.5141.67)

This $141.67 is the cost of using the tool this month.

Step 3: Cash Flow at Work

Now, the velocity part kicks in. On payday, Sarah’s entire $6,000 paycheck is deposited directly into her HELOC.

- HELOC Balance after Paycheck: $20,141.67 – $6,000 = $14,141.67

Throughout the month, she uses her HELOC like a checking account to pay her $4,500 in expenses.

- HELOC Balance at End of Month: $14,141.67 + $4,500 = $18,641.67

Step 4: The New Balances and The “Aha!” Moment

At the end of the first month, let’s look at the results:

- Her mortgage principal is down by a massive $20,000.

- Her HELOC balance is $18,641.67, which is $1,358.33 less than her original $20,000 chunk (the difference is her $1,500 cash flow surplus minus the $141.67 in HELOC interest).

She has effectively converted a huge piece of her slow-moving, 30-year mortgage into a smaller, more flexible debt that her monthly cash flow is actively and rapidly paying down. This is the core function a heloc accelerated mortgage payoff calculator is designed to model. Over the next several months, her cash flow surplus will continue to shrink the HELOC balance until it’s low enough for her to feel comfortable taking another “chunk” to attack the mortgage again.This is the core function a heloc accelerated mortgage payoff calculator is designed to model. Over the next several months, her cash flow surplus will continue to shrink the HELOC balance until it’s low enough for her to feel comfortable taking another “chunk” to attack the mortgage again.

Is Velocity Banking Worth It? The Unbiased Pros and Cons

This strategy sounds powerful, and it can be. But it is absolutely not for everyone. Before you get too excited, you need to stare the risks right in the face. Understanding these trade-offs is more important than any calculation.

| The Powerful Advantages (The Pros) | The Serious Disadvantages of Velocity Banking (The Cons) |

| Drastically Reduced Interest: By systematically eliminating principal, you can save tens or even hundreds of thousands in mortgage interest over the life of the loan. | Requires Extreme Discipline: You must treat the HELOC like a financial tool, not a slush fund. One unplanned vacation or shopping spree can erase your progress and dig you deeper into debt. |

| Faster Equity & Freedom: Paying off your home years or decades early provides immense financial security and freedom to pursue other goals. | Variable Rate Risk: If market rates rise, your HELOC interest rate will too. This can dramatically increase the cost of the strategy and eat into your cash flow. |

| Increased Liquidity: Your home equity becomes more accessible. Instead of being locked up, it’s available via the HELOC for true emergencies or other investments. | Complexity and Mental Overhead: This isn’t a “set it and forget it” plan. It requires constant monitoring, budgeting, and a solid understanding of the numbers. |

| Financial Consolidation: All your finances flow through one account, which can simplify tracking for some people. | Potential for More Debt: If mismanaged, you can end up with a large mortgage and a maxed-out HELOC, putting you in a far worse position than when you started. |

Velocity Banking Calculators vs. Reality: Apps, Spreadsheets, and Red Flags

Given the complexity, it’s no wonder people search for a velocity banking calculator app or a pre-made spreadsheet. These tools promise to simplify the process, but it’s vital to approach them with healthy skepticism.

The Allure of a Tool

A good velocity banking app or spreadsheet automates the month-by-month calculations we just did manually. It can project outcomes over years, showing a potential payoff date and total interest saved. This can be incredibly motivating and helpful for visualizing the long-term goal. Many people look for a free velocity banking calculator to get started, and some can be useful for basic modeling.

Common Red Flags to Watch For

Unfortunately, the space is also filled with misinformation and overpriced tools. Be wary of any calculator or service that:

- Downplays HELOC Interest: Some models conveniently forget to add the cost of HELOC interest, making the results look far more spectacular than they really are.

- Guarantees Results: No financial strategy is guaranteed. The market changes, and your life changes. Any tool promising a specific outcome is selling hype, not sound financial advice.

- Charges High Fees for a Simple Spreadsheet: You can find many discussions on a velocity banking calculator Reddit thread where users share free spreadsheet templates (velocity banking spreadsheet xls). Be cautious of services charging hundreds of dollars for what is essentially a pre-filled Excel file. The “Vanntastic” spreadsheet is often mentioned, but always evaluate if a paid tool offers more value than the free resources available.

Can You Use a Credit Card Instead of a HELOC?

This is a common question, especially for those without home equity. While technically possible, using a velocity with credit card strategy is exceptionally risky. Credit card interest rates are typically much higher than HELOC rates, and the fees can be astronomical. The interest costs would likely overwhelm any benefit from the principal reduction on your primary debt. For the vast majority of people, this is not a viable or advisable path.

Frequently Asked Questions (FAQ)

What is the velocity method of banking?

It’s another term for velocity banking. It refers to the strategy of using a line of credit to accelerate the payoff of amortized loans by increasing the “velocity” of money moving against the principal.

Does velocity banking cost money to set up?

Yes, potentially. Opening a HELOC can come with setup fees, appraisal costs, and annual fees, depending on the lender. These costs need to be factored into your overall calculation.

Who created velocity banking?

The concept has been around for decades under various names, like “mortgage acceleration.” It was popularized in the early 2000s by figures like Nelson Nash (in his “Infinite Banking” concept, which is different but related) and later by financial coaches and online influencers.

How does this compare to just making extra mortgage payments?

Making bi-weekly or extra monthly payments is a fantastic, low-risk way to pay off your mortgage early. Velocity banking is a higher-risk, potentially higher-reward strategy. It leverages debt to pay off debt, which offers more powerful acceleration but also introduces the risk and cost of the HELOC.

The Final Verdict: Is The Knowledge Your Best Calculator?

In your search for a velocity banking calculator, you were looking for an answer. But the real answer isn’t a number spit out by a machine. It’s a deep understanding of your own finances, your discipline, and your tolerance for risk.

The strategy is not a myth, but it’s also not magic. It is a powerful tool for the financially savvy and disciplined individual who can manage cash flow meticulously and respect the risks of leverage.

By walking through the math yourself, you’ve done something more valuable than any automated calculation. You’ve empowered yourself. You now have the single best tool there is: the knowledge to look at your mortgage, your income, and your goals, and decide for yourself if this is the path that will lead you to financial freedom faster.